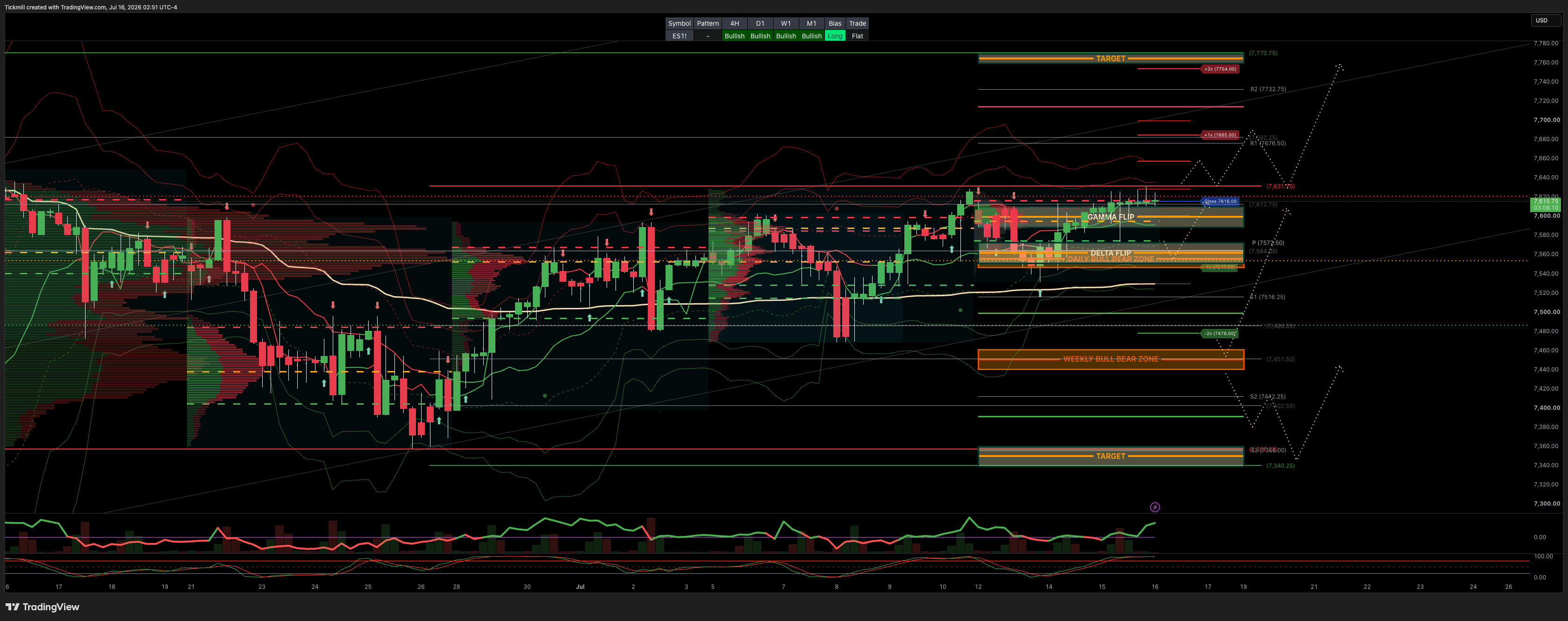

S&P500 Daily Action Areas & Price Targets 16/7/26

S&P500 Daily Action Areas & Price Targets 16/7/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7460/40

WEEKLY RANGE RES 7710 SUP 7530

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q3 Collar Short Call Cap: ~7,750 – 7,900 - Long Put Strike: ~7,050 – 7,100 (approx. 5% downside protection) Short Put Strike: ~5,950

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.4 (The numbers reflect options traded during the current session.) A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish.

GS Flow Desk: large S&P 31Aug 7000/7950 strangle in roughly $20mm vega / $115mm premium …My Read – classic “big convexity versus carry” trade: either someone paid a lot to own a wide August move, or someone got paid a lot to bet that the S&P stays comfortably inside the 7000–7950 corridor

DAILY VWAP BULLISH 7596

WEEKLY VWAP BULLISH 7527

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - BALANCE 7627/7469

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7540/50**ACTIVE FROM RECLAIM**

GAMMA FLIP 7599

DELTA FLIP 75

DAILY RANGE RES 7685 SUP 7547

2 SIGMA RES 7754 SUP 7478

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL/BEAR ZONE TARGET DAILY RANGE RES***ACTIVE***

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS FICC & EQUITIES TRADING DESK VIEWS

US Equities Color — Benign Inflation, Hyperscaler Rotation, Semi Frustration

US equities finished modestly higher, supported by another benign inflation print, lower yields, a weaker dollar, and strong demand for hyperscalers, even as the AI momentum trade remained choppy under the surface. The S&P 500 rose 38bps to 7,572, the Russell 2000 gained 36bps to 2,975, and the Dow added 29bps to 52,658. The NDX lagged, falling 28bps to 29,502, weighed down by semiconductor and memory weakness despite strength in hyperscalers and AAPL.

The close saw a sizeable $4.9bn MOC to buy, and the floor finished +60bps better to buy versus a 30-day average of +29bps. Activity remained muted, however, with the floor at only a 4 out of 10 and total US equity volume of 16.263bn shares versus a YTD daily average of 19.538bn. The tape remains a thin-liquidity summer market, where large rotations can happen beneath relatively calm index-level moves.

Cross-asset conditions were broadly equity-friendly. VIX fell 485bps to 15.70, WTI rose 130bps to $80.37, the US 10-year yield declined 4bps to 4.5493%, gold was roughly flat at 4,056, DXY fell 40bps to 100.51, and Bitcoin rose 60bps to $64,916. The key macro message was that disinflation data continue to improve, while energy remains the persistent offset.

Macro — PPI Adds to the Benign Inflation Narrative

The macro backdrop improved again after a softer-than-expected June PPI report. Headline PPI declined in June, while core PPI and PPI excluding food, energy, and trade services increased only slightly, all below expectations. Combined with the earlier CPI data, this supports the view that near-term inflation pressure is easing.

Following CPI and PPI, GS now estimates that core PCE rose 0.17% in June, slightly below the prior estimate of 0.18%, corresponding to a year-over-year rate of 3.32%. Market-based core PCE is estimated at 0.19% for June.

That matters because the market had recently been wrestling with the risk of renewed Fed tightening, especially after hawkish Waller commentary. The softer CPI/PPI sequence has pushed the first expected hike out to December, relieving immediate pressure on equities and helping the 10-year yield ease to around 4.54%.

The caveat remains oil. WTI is now above $80, keeping inflation tail risk alive despite the softer June data. For now, the market is treating the oil move as manageable and possibly geopolitical/temporary, but a sustained move higher would eventually challenge the disinflation narrative and pressure consumer-facing margins.

Index Tape — Calm at the Surface, Rotational Underneath

The S&P closed higher at 7,572, keeping the index comfortably above the important short-term CTA pivot at 7,427. That is constructive from a systematic-flow perspective. As long as the S&P remains above that level, the baseline CTA flow setup remains supportive rather than forced-selling-oriented.

However, the headline index move understated the degree of dispersion below the surface. The NDX finished lower despite the broader market rally because the AI complex split sharply between hyperscalers / AAPL strength and semiconductor / memory weakness. This is now the dominant market dynamic: the AI trade is not being abandoned, but capital is rotating aggressively within it.

AI / Tech — Hyperscalers Bought, Semis Sold

The main equity story was the continued divergence inside AI and tech. The momentum wobble was triggered by underwhelming price action after the ASML print. Fundamentally, ASML’s guidance was strong: FY26 revenue guidance came in more than 10% above the Street, with upbeat forward commentary. But the stock reaction and broader semicap/memory performance disappointed investors.

That kind of price action is important. When a company delivers good news and the stock still trades poorly, it usually tells us the issue is not the immediate print but positioning, expectations, and prior ownership. The market had already crowded into semicap equipment and memory, so even positive guidance was not enough to support the group.

Desk observations from the tech pad were telling:

There was a notable uptick in client frustration around semiconductor moves, especially memory and semicap equipment.

There was a huge divergence between hyperscalers + AAPL, up roughly 3–5%, and semis, down roughly 2–8%.

The desk was extremely active buying hyperscalers for the long-only community.

Semi high-touch activity was less active, but flows skewed better for sale.

This reinforces the rotation theme discussed in recent sessions: investors are increasingly reallocating from crowded AI infrastructure suppliers toward platform winners and hyperscalers, where positioning has reset and valuation/revision risk looks more balanced.

Mag7 and Hyperscalers — Re-Accumulation Underway

The Mag7 basket outperformed the NDX by around 2.5%, helped by strong demand for hyperscalers and AAPL. That is notable because positioning in the group has come in materially. After several weeks of de-risking and rotation away from the most crowded mega-cap tech exposure, investors appear more willing to re-enter selectively.

The long-only community was extremely active buying hyperscalers. This is a more durable demand signal than pure hedge fund short covering. It suggests fundamental investors are using the recent AI/momentum correction to rebuild exposure in the cleaner parts of the trade.

The distinction is important: the market is not saying “AI is over.” It is saying the ownership and expectations bar was too high in semis/memory/semicap, while the hyperscalers now look comparatively cleaner.

Momentum — Correction Nearing Exhaustion?

Momentum closed lower despite the broader market rally. That remains a concern, but the desk view is turning more constructive. After an estimated 60–70% reduction in AI holdings within the hedge fund community over the past 5–6 weeks, the desk thinks this is a good time to re-enter.

The view is that the momentum correction is likely nearing its end. That does not mean every crowded AI name immediately works. Rather, it suggests the forced-positioning unwind may be closer to completion, creating opportunities to rotate into cleaner winners.

The recommended expression is to rotate from over-played Mag7 names into META upside. The logic is that META offers a cleaner upside profile versus some of the more heavily played mega-cap tech names, especially if AI monetization, ad strength, and capex discipline remain favorable.

Derivatives — Vol Offered, but Index Hedges Still Active

Derivatives activity showed a split between lower implied vol and continued demand for protection. S&P fixed-strike vols were offered across the surface, and skew was crushed, most notably in the front end. This fits the macro backdrop: softer inflation, lower yields, less immediate Fed risk, and a calmer index tape.

At the same time, the desk continued to see meaningful index hedging. Buyers of 2-month S&P put spreads traded in larger size both yesterday and today. That suggests investors are using lower vol and flatter skew to add protection into the earnings window rather than chasing the rally unhedged.

This remains sensible. The market is near highs, earnings expectations are elevated, oil is above $80, semis are unstable, and liquidity is poor. Even with spot higher and vol lower, protection still screens attractive versus the catalyst set.

Futures buying was also notable out of the gates, with volumes 11% above the 5-day moving average. That helped support the index level, even as single-name dispersion remained significant.

Implied Range Projection

The implied move for the rest of the week went out at approximately 64bps. With the S&P closing at 7,572, that implies a move of roughly:

Rest-of-week implied SPX range: 7,523 to 7,621.

This is a constructive range because the lower end, 7,523, is comfortably above the short-term CTA pivot at 7,427. The market is no longer pricing a normal move toward the CTA trigger this week. A break below 7,523 would indicate the tape is moving beyond the priced range, while a break below 7,427 would be the more important systematic-flow warning level.On the upside, 7,621 would mark a fresh extension into record-high territory. To get there, the market likely needs continued yield relief, no further oil shock, stabilization in semis, and constructive earnings follow-through.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!